Buying an RV sounds exciting until the numbers step in. A large down payment, strict loan approvals, and long-term commitments can slow things down quickly.

So the idea of renting your way into ownership feels like a smart workaround. No heavy upfront cost. Fewer barriers. You get the RV now and figure out the rest along the way.

But here is the part most buyers do not stop to question. If it is easier to get, is it actually better for your budget?

For many, rent-to-own looks like a flexible path. In reality, it can quietly become a more expensive one.

If you are trying to make a careful financial decision, it is worth taking a closer look before you commit.

Key Takeaways

- Rent-to-own RV agreements offer an alternative for buyers who cannot qualify for traditional financing due to low credit or limited savings.

- This option requires little to no down payment, but the overall cost of ownership is significantly higher compared to bank loans.

- Payments are typically more frequent and include both rental and principal components, making financial planning essential.

- Buyers are usually responsible for maintenance, insurance, and storage costs, even before full ownership is transferred.

What's Rent To Own?

Rent-to-own is an option that allows buyers to work toward RV ownership without going through traditional RV financing. It is often considered by those who may not qualify for a bank loan due to a low credit score or limited savings.

In most cases, standard RV loans require a down payment, strong credit history, and defined loan terms. Rent-to-own works differently. Instead of relying on a lender, you enter into a lease-to-own agreement with a dealer or a private owner, usually with fewer upfront requirements such as proof of income and residence.

Under this agreement, your monthly payments are split into two parts. One portion goes toward the purchase price of the RV, while the other covers the cost of using it. Once all contract terms are met, ownership is transferred to you.

The Pros And Cons Of Rent To Own

Not everyone can qualify for bank financing or pay cash for an RV. If you're ready to buy an RV, but your financial circumstances require alternate financing, then renting to own an RV might be for you.

However, before entering any agreement, it is important to weigh both the advantages and the tradeoffs carefully.

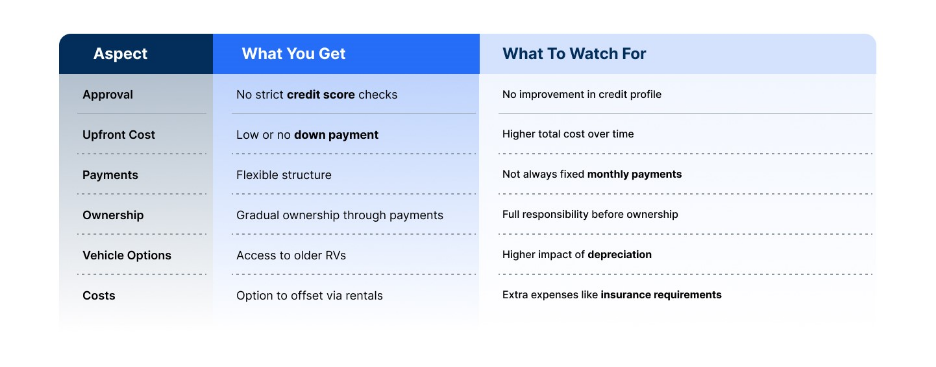

Pros

No Credit Check Required: Most rent-to-own agreements do not rely heavily on your credit score, making them accessible if you have faced loan rejections or financial setbacks.

Little Upfront Cost: Many rent-to-own agreements ask for little to no down payment, which can make it easier to get started without significant savings.

Access To Older RVs: Traditional lenders often avoid financing older vehicles due to depreciation concerns. Rent-to-own gives you more flexibility in choosing older or vintage models.

Flexible Seller Terms: Dealers and private sellers may offer more adaptable contract terms, especially when they are motivated to sell quickly.

Opportunity To Offset Costs: Some RV owners explore peer-to-peer rental platforms to generate income when their RV is not in use. This can help offset ownership costs over time, but it operates independently of any rent-to-own arrangement.

Cons

Higher Overall Cost: Since the seller is not a traditional lender, your payments often exceed what you would pay under standard RV financing, especially when factoring in informal rates similar to a high APR.

Frequent Payment Schedules: Instead of structured monthly payments, many agreements require weekly or bi-weekly payments, which can strain cash flow.

Full Maintenance And Ownership Costs: Many rent-to-own contracts require you to pay for all maintenance and repairs as if you purchased the RV outright. Also, since you're using the RV as if it were your own, you'll still have to pay for storage and insurance.

No Credit Reports: Rent-to-own contracts don't typically report your on-time payments to the bank. Since your lease doesn't require financing, the owner has no reason to contact the bank. A rent-to-own contract might not be for you if you're trying to re-establish credit.

No Refund Flexibility: If you choose to exit the agreement, you may lose the portion of payments that went toward usage rather than ownership.

The Cost Of Renting-To-Own An RV

When you choose a rent-to-own option, your payments go directly to the dealer or private owner instead of a bank or lender. While there is no formal loan involved, the structure still divides your payment into two parts, one that contributes toward ownership and another that covers usage.

These payments are often higher because they are not regulated like traditional financing. In many cases, the cost structure can resemble informal dealer financing, where pricing is set by the seller rather than tied to standard market rates.

Most agreements also require an upfront commitment, typically including the first and last payments instead of a traditional loan setup. The contract terms are usually shorter, often between 48 and 60 months, which means you are paying off the vehicle faster.

Some agreements may also include conditions similar to balloon payments, where a larger final amount is due at the end of the term to complete ownership. This is an important detail to review before signing, as it can significantly impact the total cost.

Pro Tip: Before signing any agreement, calculate the total amount you will pay over the full term and compare it with other options like personal loans or standard financing. This gives you a clearer picture of whether the convenience is worth the extra cost.

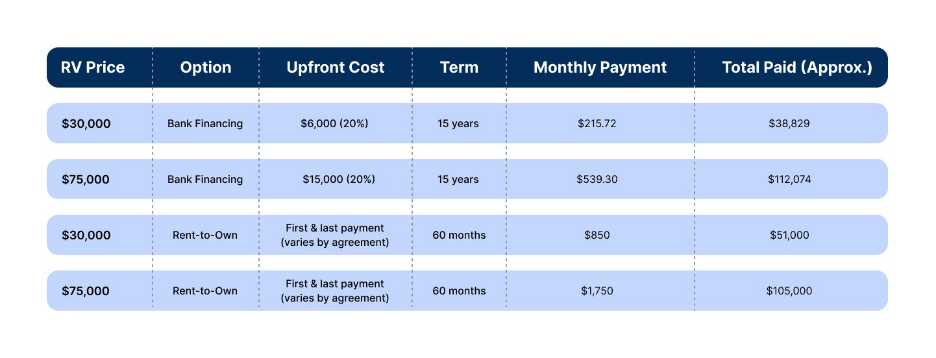

Comparing RV Financing vs Rent-to-Own Costs

To accurately compare both options, it is important to separate structured bank lending from contract-based rent-to-own agreements. Bank financing follows a regulated loan model with interest, down payments, and amortization. Rent-to-own, on the other hand, is a fixed payment agreement set by the seller, typically without formal lending terms or credit reporting.

The table below reflects corrected loan math for bank financing and verified contractual totals for rent-to-own structures.

Extra costs

As with traditional RV financing, you'll still have to pay tax, registration, and licensing fees when you rent to own an RV. In addition, you will have to pay for insurance, storage, maintenance, and other costs associated with RV ownership.

Even though you'll be responsible for the cost of ownership, it doesn't hurt to ask if the owner offers maintenance packages, roadside assistance, or has a place to store your RV. Motivated owners might add in something that will benefit both of you.

What To Look For In A Rent-To-Own RV Lease

If you are considering a rent-to-own agreement, reviewing the details carefully can help you avoid unexpected costs and long-term financial strain. These agreements often vary from seller to seller, so it is important to understand exactly what you are signing.

Here are the key factors to evaluate before committing:

- Total Purchase Price: Confirm the full payout amount of the RV, not just the periodic payments. This helps you understand the actual cost of ownership.

- Upfront Costs And Fees: Check for any required deposits, advance payments, or late fees that may increase your overall expense.

- Payment Structure: Review the payment amount, due dates, and frequency. Ensure the schedule fits your cash flow and aligns with your financial planning.

- Contract Duration: Understand the length of the agreement. Shorter durations may lead to higher payments, while longer ones may increase the total cost.

- Principal Allocation: Clarify how much of each payment goes toward ownership versus usage. This directly affects how quickly you build equity.

- Early Payoff Terms: Look for any penalties or benefits tied to early repayment. Some agreements may limit flexibility if you want to close the deal sooner.

- Default Conditions: Understand the consequences of missed payments. This includes penalties, repossession terms, and loss of previously paid amounts.

- Insurance Requirements: Review the minimum insurance requirements outlined in the agreement to avoid compliance issues or unexpected costs.

- Included Benefits: Check if the agreement includes extras such as maintenance support or storage, which can reduce your ongoing expenses.

Common Mistakes To Avoid

Rent-to-own agreements can seem straightforward, but many buyers overlook key details that directly impact long-term cost and financial flexibility. Paying attention to these areas can help you avoid costly decisions.

- Focusing Only On Short-Term Affordability: It is easy to prioritize manageable payments without evaluating the total payout. Rent-to-own often spreads costs in a way that feels affordable now but increases the overall amount paid.

- Not Comparing With Other Financing Options: Skipping a comparison with traditional RV financing or personal loans can lead to overpaying. Even with a moderate APR, structured financing may still be more cost-effective.

- Overlooking The Impact Of Depreciation: RVs lose value over time due to depreciation. If your total payments exceed the vehicle’s actual market value at the end of the term, you are paying more than what it is worth.

- Not Understanding Payment Allocation: Many buyers do not clearly track how much of each payment goes toward ownership versus usage. This can slow down equity buildup and delay full ownership.

- Ignoring Contract Details And Penalties: Incomplete review of contract terms can result in unexpected charges, late fees, or strict penalties for missed payments. Some agreements may also include clauses similar to balloon payments, increasing your financial obligation later.

Frequently asked questions

Can I finance an RV with bad credit?

Financing an RV with bad credit can be challenging. If you’re worried that bad credit may make it impossible to finance an RV, renting to own may be an option.

Can you rent to own an RV with no down payment?

In most cases, rent-to-own agreements do not require a traditional down payment. This is one of the main reasons they appeal to buyers who may not have significant savings upfront.

However, this does not mean you can start without any initial cost. Most sellers require an upfront commitment, typically the first and last payment, before you can take possession of the RV. While this structure reduces the need for a lump sum, it still involves an initial financial outlay that you should plan for in advance.

Can I pay monthly for an RV?

Yes! The whole point of rent to own is that you have monthly payments where part of your payment will go toward the total purchase price, and part of the payment will cover rental fees.

Is it cheaper to rent an RV or buy one?

In most cases, renting an RV is cheaper in the short term, while buying becomes more cost-effective only if you use it frequently.

How do I find a rent-to-own RV?

You can explore rent-to-own arrangements primarily through local RV dealerships or by negotiating directly with private sellers. Rent-to-own RV agreements are usually not listed as standard offers. They are typically arranged directly with RV dealers or negotiated with private sellers. It is important to review contract terms carefully before committing to any deal.

Team RVezy

Team RVezy is a group of RV enthusiasts who traverse the U.S. and Canada in our campervans, tiny trailers, and motorhomes. We love the open road and the feeling of having nowhere to go but everywhere.

View more posts